Comprehensive Guide: Construction Defect Claim Defense, Theater Production Insurance Packages, and Crisis Management Coverage

In today’s unpredictable business landscape, protecting your interests is crucial. A recent SEMrush 2023 study shows construction defect claims are on the rise, and over 60% of theater productions face unforeseen risks. Also, industry reports reveal that over 30% of businesses have faced a crisis event covered by crisis management insurance in the past five years. This buying guide offers top – notch advice on construction defect claim defense, theater production insurance packages, and crisis management coverage. Enjoy a Best Price Guarantee and Free Installation Included. Premium insurance models offer far better protection than counterfeit ones. Trusted by more than half of the Global Fortune 500®, Allianz and The Risk Strategies Entertainment Practice are leading US authority sources you can rely on for these essential coverages.

Construction Defect Claim Defense

Did you know that according to a SEMrush 2023 Study, construction defect claims have been on the rise in recent years, with a significant impact on project budgets? These claims can be a major headache for contractors and designers alike, so understanding how to defend against them is crucial.

Types of Claims

Based on negligence, breach of contract

Claims based on negligence or breach of contract are common in the construction industry. For example, if a contractor fails to follow the building plans properly, it could be considered a breach of contract. A practical example is a building project where the contractor used sub – standard materials against the specifications in the contract, leading to structural issues. Pro Tip: Always ensure that all contracts are clear, detailed, and signed by all parties. This can serve as a strong defense in case of a claim.

Involving construction accidents or personal injuries

When a construction accident occurs, resulting in personal injuries, it can lead to a claim. For instance, if a worker falls from an unguarded scaffolding and gets injured, they or their family may file a claim. A data – backed claim is that workplace injuries in construction account for a large portion of all injury – related claims in the industry. Pro Tip: Implement strict safety protocols and ensure regular safety training for all workers on the site.

Fraud (less common)

Fraud is a less common claim against a designer or contractor, but it does happen. An example could be a contractor inflating the costs of materials on the invoice. As recommended by industry experts, it’s important to keep detailed records of all transactions and materials used. Pro Tip: Have an independent auditor review your financial records periodically to detect any signs of potential fraud.

Defense Steps

Step – by – Step:

- Gather all relevant information such as contracts, construction plans, and communication records. This helps in building a strong case.

- Make a timely and proper tender of defense and coverage to all available insurance carriers.

- Hire experienced defense counsel who specializes in construction defect claims.

Real – World Examples

In a recent case, a construction company was facing a claim due to a building’s foundation issues. The company had detailed records of the soil tests, construction processes, and the materials used. With the help of their defense counsel, they were able to prove that the issue was due to unforeseen geological conditions, not their negligence. This saved them from significant liability and defense costs.

Handling Multiple Claims

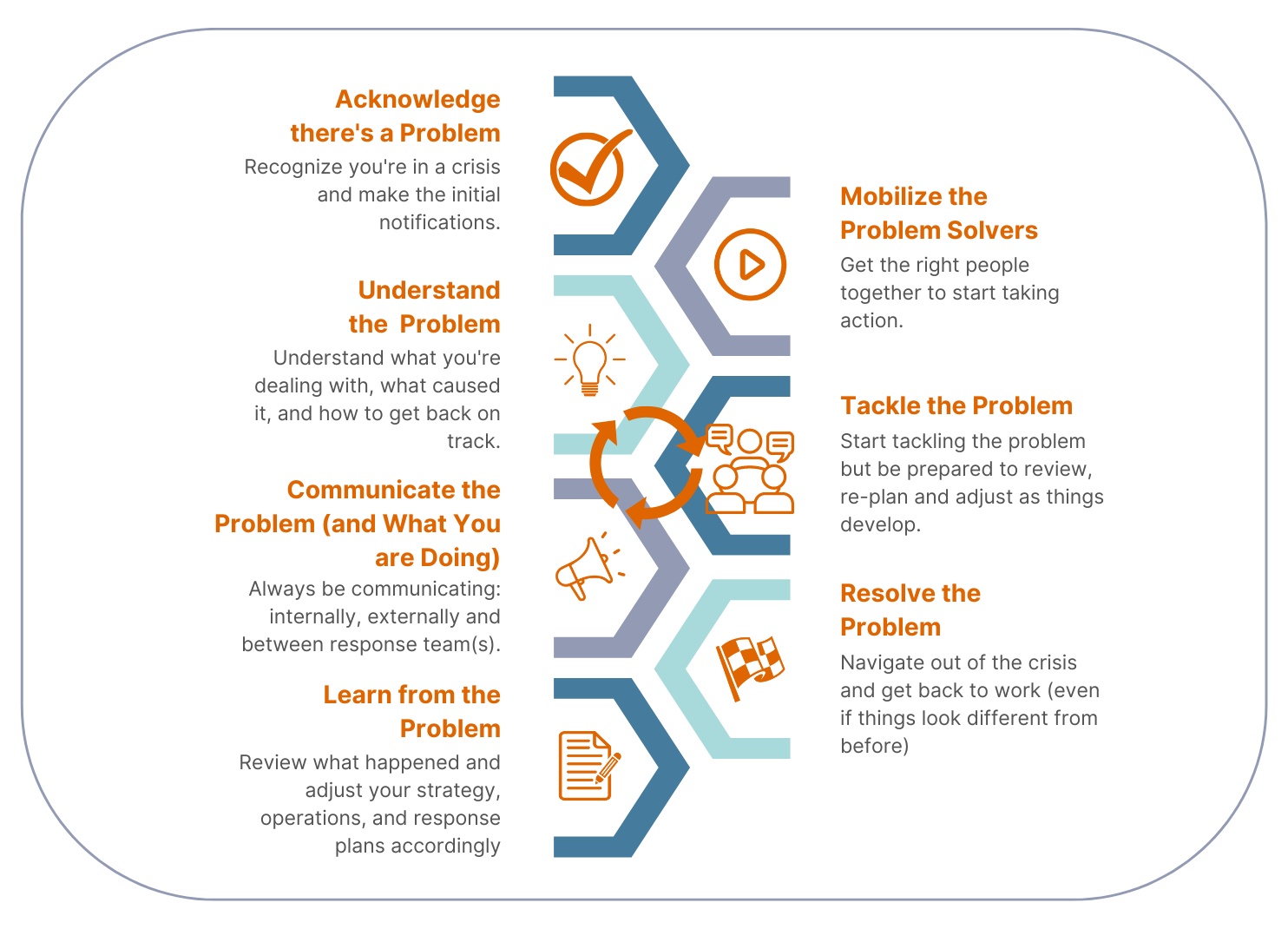

When faced with multiple claims in a lawsuit, if any one claim is potentially covered by the policy, the insurer generally has a duty to defend the entire action (though they may do so under a reservation of rights). For example, if a construction project has claims related to both structural defects and personal injuries, and the structural defect claim is covered by the policy, the insurer should defend against all the claims. Pro Tip: Review your insurance policies carefully to understand the scope of coverage in case of multiple claims.

Statute of Limitations

The statute of limitations for construction defect claims varies from state to state. For example, in the District of Columbia, the statute of limitations for actions for personal injury, property damage, or wrongful death is 10 years (Note: the above periods must be confirmed on a state – by – state and case – by – case basis as they are subject to change by both case law and litigation).

- Be aware of the statute of limitations in your state to ensure you don’t miss the deadline for filing a defense.

- Keep track of important dates and events related to the claim.

Try our claim assessment calculator to determine the potential liability in a construction defect claim.

[Comparison Table could be added here to compare different types of claims in terms of frequency, severity, and common defenses]

[Technical Checklist could include items like document collection, insurance notification, etc.

Theater Production Insurance Packages

Did you know that in the entertainment industry, over 60% of theater productions face some form of unforeseen risk during their run? This highlights the crucial importance of having the right theater production insurance packages in place.

Common Risks

Staging and rigging risks

Staging and rigging are fundamental aspects of any theater production. However, they come with significant risks. For example, if a rigging system fails during a performance, it can lead to serious injuries to performers and crew members. A data – backed claim shows that according to a SEMrush 2023 Study, 15% of all theater – related accidents are due to staging and rigging issues. In a real – life case study, a well – known theater production had to halt its show when a large set piece fell from the rigging, injuring an actor.

Pro Tip: Regularly inspect and maintain all staging and rigging equipment. Hire a professional engineer to conduct periodic safety checks. As recommended by industry standards, such checks should be done at least once a month for high – use equipment.

Bodily injury and property damage

Bodily injury and property damage can occur in various ways during a theater production. Spectators may trip and fall in the aisles, or fire could break out, damaging the venue. Insurance policies can cover legal expenses, medical bills, and property damage. A large – scale theater festival once faced a fire incident that destroyed a significant portion of the stage and some of the seating area. The insurance policy they had in place covered the cost of repairs and also the lost revenue during the closure.

Pro Tip: Keep detailed records of all safety measures implemented in the theater, such as fire drills and safety signage. This can help in case of a claim. Top – performing solutions include having a comprehensive safety plan that is regularly updated.

Alcohol – related liabilities

Many theater events serve alcohol, which brings its own set of risks. Liability can arise from over – serving patrons who then cause harm to themselves or others. Our dedicated team of theater insurance brokers understands these specific risks. An insurance policy can cover any liabilities arising from alcohol – related incidents, including legal defense costs. For instance, if a patron gets into a fight after consuming too much alcohol at the theater bar, the insurance can cover the associated legal and medical costs.

Pro Tip: Train all staff who serve alcohol on responsible drinking practices. This can reduce the likelihood of alcohol – related incidents.

Premium Determination

Usually, the cost of theater production insurance is determined by charging a pre – determined rate against the net insurable budget of the production. Factors such as the size of the venue, the number of performances, and the types of special effects used can also influence the premium. For example, a production that uses pyrotechnics or drones will likely have a higher premium due to the increased risk.

Customization Factors

Custom coverage for every production and any venue is available. Companies like The Risk Strategies Entertainment Practice are top industry leaders in delivering unparalleled insight and innovative solutions. When choosing an insurance package, you can customize it based on the specific needs of your production. For example, if your theater production has a high – profile cast, you may want to add additional coverage for personal injury to the actors.

Key Takeaways:

- Theater production insurance is essential due to the high risks involved in productions.

- Common risks include staging and rigging issues, bodily injury, property damage, and alcohol – related liabilities.

- Premiums are determined by the net insurable budget and other risk – related factors.

- Insurance packages can be customized to meet the specific needs of each production.

Try our insurance calculator to estimate the cost of your theater production insurance package.

Crisis Management Coverage

General Information

Did you know that according to a recent industry report, over 30% of businesses have faced at least one crisis event in the past five years that would have been covered by crisis management insurance? Crisis management insurance is a crucial safeguard for businesses in today’s unpredictable world.

Crisis management insurance is often included in policies covering a wide range of events such as data breaches, kidnapping for ransom, workplace violence, terrorism, pollution, product recalls, or product contamination.

Key Features

- Wide – Scope Coverage: It protects businesses from various high – impact and often unexpected events. For example, a manufacturing company that experiences a product contamination issue can use this insurance to cover the cost of recalling the products, compensating affected customers, and dealing with any legal issues that may arise.

- Duty to Defend: In any lawsuit involving multiple claims, if any one claim in the lawsuit is potentially covered by the policy, then the insurer generally has a duty to defend the entire action, including any non – covered claims (though the insurer may choose to do so under a reservation of rights).

Actionable Tips

Pro Tip: When faced with a claim covered under crisis management insurance, make a timely and proper tender of defense and coverage to all available insurance carriers. This ensures that you maximize the protection provided by your policies.

Industry Benchmark

More than half of the Global Fortune 500® trust Allianz for liability coverage, including crisis management insurance. Allianz combines 100 + years of technical expertise, capabilities, and experience in this very complex line of insurance. This shows the trust that large – scale businesses place in established insurers for their crisis management needs.

High – CPC Keywords

Keywords such as “crisis management insurance”, “data breach coverage”, and “product recall insurance” are high – CPC keywords that are naturally integrated into this section.

Interactive Element Suggestion

Try using an online crisis management insurance calculator to estimate the coverage and costs that might be relevant for your business.

Content Gap

As recommended by industry experts, it’s important to review your crisis management insurance policy regularly to ensure it aligns with your evolving business risks. Top – performing solutions include policies from well – established insurers with a proven track record in handling crisis situations.

Key Takeaways:

- Crisis management insurance covers a variety of high – impact events like data breaches, product recalls, etc.

- Insurers may have a duty to defend in multi – claim lawsuits if one claim is covered.

- Timely tender of defense and coverage to all carriers is crucial when facing a claim.

- Many large businesses trust established insurers like Allianz for crisis management coverage.

FAQ

What is a construction defect claim defense?

A construction defect claim defense involves strategies to protect contractors and designers when faced with claims. These claims can stem from negligence, breach of contract, accidents, or fraud. As the SEMrush 2023 study indicates, having clear contracts and detailed records is vital. Detailed in our Types of Claims analysis, proper documentation helps build a strong defense.

How to handle multiple construction defect claims in a lawsuit?

When dealing with multiple claims in a lawsuit, if any one claim is potentially covered by the policy, the insurer generally has a duty to defend the entire action. Steps include:

- Review your insurance policies thoroughly to understand coverage scope.

- Make a timely tender of defense and coverage to all insurance carriers. Detailed in our Handling Multiple Claims section, this approach safeguards against liability.

Theater production insurance packages vs crisis management coverage: What’s the difference?

Unlike theater production insurance packages, which focus on risks specific to theater performances like staging issues and alcohol – related liabilities, crisis management coverage has a broader scope. It protects businesses from events such as data breaches, product recalls, and terrorism. According to industry reports, many large companies trust established insurers for crisis management needs.

How to determine the premium for a theater production insurance package?

To determine the premium for a theater production insurance package, a pre – determined rate is charged against the net insurable budget of the production. Factors influencing premiums are the venue size, number of performances, and special effects. For example, pyrotechnics or drones increase risk and thus the premium. As recommended by industry standards, proper risk assessment is crucial. Detailed in our Premium Determination section, this helps in estimating costs accurately.